In its second survey, Binance Research analyzed typologies and views from the most significant VIP and institutional clients, who had been using some of the services offered within the Binance ecosystem.

Out of nearly 200 parties we contacted, our final client sample size totaled 76 participants across our English & Mandarin surveys, primarily composed of firms, funds, and institutions with respective allocations to cryptoassets ranging from $100K to more than $25M.

A majority of our clients entered the cryptoasset industry following years of conventional financial industry work experience. Over a quarter of respondents have 7+ years of traditional finance experience and the vast majority of the respondents 1 to 3 years in the crypto-space under their belt.

The three most commonly followed investment strategies were high-frequency prop trading (35.5%), technical analysis (25.0%), and market-making (19.7%).

54% of respondents kept their cryptoasset portfolio between 1-10 coins, a characteristic reflected across all investment and trading strategies.

Despite its ongoing legal issue being considered one of the most significant risks for the industry, USD Tether (USDT) remained the most widely used stablecoin (40%), for reasons quoted such as greater liquidity and higher market capitalization than its peers. While alternative options are also being used, stablecoins backed by exchanges, like USDC (Coinbase, Circle) and BUSD (Binance), seemed to spark more prominent interest from many respondents than other (than USDT) fiat-backed competitors.

Regulations remained one of the critical aspects of interest, both as a risk and a potential growth driver for the future of this industry. Meanwhile, sophistication on the product side was viewed positively by participants as ETFs, derivatives, and brokerage services were ranked as top potential growth drivers for the cryptoasset industry.

Clients do not consider Libra, nor CBDC, to present a risk for the industry, and many even ranked them as growth drivers. Privacy concerns do not seem to spark any (positive or negative) reaction from any crypto-client. In a similar vein, neither decentralized exchanges nor lending services, appeal to the majority of these large clients. Conversely, staking has picked up interest, conceivably as it operates at the protocol level while lending relies on trust (either to a smart contract code or to a third-party).

Finally, institutional and VIP clients expected Bitcoin to maintain a considerable market dominance (69%) by the end of 2019, which echoes their fear of the altcoin market, losing any interest from retail participants.

In October 2019, Binance Research conducted its second survey distributed to large institutional and VIP clients using Binance’s wide range of services such as exchange platforms and OTC trading desk.

This report was prepared in cooperation with Binance Trading, one of the world’s largest liquidity pools, for institutional and VIP clients involved in the digital asset industry1.

This report was prepared in cooperation with Binance Trading, one of the world’s largest liquidity pools, for institutional and VIP clients involved in the digital asset industry1.

Following our first report on institutional market insights, we discuss key results and findings stemming from these collected responses, while putting them in perspective with historical figures.

1. Typologies and experiences

Over one hundred of our institutional and VIP clients were selected and contacted by email or direct message with a link to complete this survey. Response data were collected anonymously to encourage open sharing of perspectives and opinions.

Our final respondent sample size for this survey was 76 clients, involved in the Binance ecosystem2, with a number of incomplete responses excluded. The study was conducted in two languages: Mandarin and English. Clients from these two audiences were reached in their preferred language at least twice.

Based on this relatively small sampling of client responses, we advise that the results described in the following sections should be interpreted within the context and not be generalized to the entire institutional landscape. However, it is worth noting a significant increase in the engagement of clients (+85%) compared to the previous survey, which we conducted in June 2019.

With that said, our aim with this report is to showcase a few of the invaluable insights shared by our key clients over the recent months.

1.1 Typologies of the respondents

Chart 1 - AuM/Capital allocated to cryptoasset investment or trading in USD (in % of the total responses) (74 respondents)

Our surveyed clients are stewards of investment portfolios, including cryptoasset allocations ranging from ~100K to >25M (in USD). They represent a diverse set of perspectives from independent traders, proprietary trading firms, investment funds, crypto-project teams, investors entities, OTC brokerage firms, and sell-side financial institutions.

35% of respondents are crypto-focused with more than 80% cryptoasset allocation, while the majority also invest in a broader set of asset classes such as equities, currencies, fixed-income product, real estate, and commodities (which includes gold).

Table 1 - Past experiences in the traditional financial industry and cryptoasset industry (in % of the total responses)

How many years of experience? | Less than 1 (crypto-industry) | 1-3 (crypto-industry) | 4-6 (crypto-industry) | 7+ (crypto-industry) |

|---|---|---|---|---|

Less than 1 (financial industry) | 1% | 10% | 6% | - |

1-3 (financial industry) | - | 19% | 13% | 1% |

4-6 (financial industry) | 1% | 13% | 6% | - |

7+ (financial industry) | - | 16% | 10% | 1% |

The typical respondent has been involved in the cryptoasset industry between 1-3 years, with several years of work experience in traditional finance under their belt, as illustrated in table 1.

Chart 2 - Stablecoin use (in % of the total responses) according to clients (69 respondents)

USDT is the dominant stablecoin with 40.25% usage, holding the top ranking for both Chinese & English survey respondents. USDC, TUSD, PAX are following close behind USDT, and several English survey respondents wrote in BUSD under “Others”, reflecting an initial interest by our institutional & VIP clients. Interestingly, Chinese respondents favored USD Tether (more than half used it), while a mere 12.2% of the Chinese-speaking respondents used USD Coin(USDC). On the other hand, USD Coin was selected by nearly one-fourth of the respondents who decided to answer the survey in English.

Putting the broader results in line with respective market capitalizations, the overall use for each stablecoin is roughly in line with the rank of its respective market capitalization, as illustrated by the chart below.

Chart 3 - Stablecoin market capitalization as of October 31st 2019 in USD million

Hence, the use of stablecoins is positively tied to the circulating market capitalization of each stablecoin.

1.2 Trading strategies and investment universe

The three most popular trading strategies followed by our surveyed VIP and institutional clients were:

High-frequency prop trading (Stat arb, vol break out, ORB) with 35.5%

Technical Analysis (e.g., RSI, MACD) with 25.0%

Market making with 19.7%

Table 2 - Investment/Trading strategies based on the variety of cryptoassets traded (65 respondents)

What is your core investment/trading strategy? | 1-10 cryptoassets traded | 11-20 cryptoassets traded | 21-50 cryptoassets traded | 51+ cryptoassets traded |

|---|---|---|---|---|

High-frequency prop trading (e.g., Stat Arb, Vol. Break Out, ORB) | 8 | 4 | 6 | 5 |

Technical Analysis (e.g., RSI, MACD) | 13 | 3 | 1 | - |

Market-making | 4 | 4 | 1 | 3 |

Long-term fundamental value investment | 5 | - | - | - |

Macro long/short | 2 | - | - | - |

Rule-based rebalancing approach (e.g., equal weighting, Black Litterman) | 1 | - | - | 1 |

Others | 2 | 2 | - | - |

54% of respondents keep their cryptoasset investment/trading universe between 1-10 coins, a characteristic reflected across all investment and trading strategies. We noticed that high-frequency proprietary traders focused on a more extensive set of coins (than clients conducting other strategies), possibly owing to arbitrage-like strategies that do not require capital to remain on the order books.

On the contrary, market-making strategies requiring capital to stay on the books influenced the number of coins that they trade. Based on their respective capital allocated to cryptoassets, smaller clients traded less than 10 assets, while 10 to 20 assets were often analyzed and traded by more substantial clients.

55.2% of respondents confirmed that they reference published research reports to inform their investment decision making. Nearly all traders following long-term value investment and technical analysis strategies are reading research reports from Binance Research, Messari, CoinGecko, and other exchanges’ research desks. With that said, market-making and high-frequency prop traders do not often read research publications to guide their strategies.

Chart 4 - Trading hours according to respondents (in % of the total responses - 76 respondents)

With the borderless nature of cryptocurrency trading markets, it is only natural that the bulk of respondents are trading around the clock.

Specifically, nearly all the clients following market-making and high-frequency prop trading strategies are trading at “All hours”. Following “All hours”, the next most popular choices were respectively Asia/Oceania (32.89%) and EMEA (19.74%) time zones.

Across all levels of AuM and geographies, clients use third-party OTC desks, P2P fiat desks, and exchange OTC desks primarily as a fiat-crypto gateway (50.8%). Often cited additional reasons for using OTC services include better liquidity (26.23%), less trading hassle (16.4%), access to assets not listed on exchanges (3.3%), and the availability of alternative payment methods (1.6%).

Chart 5 - Custody and asset storage according to respondents (in % of the total responses - 76 respondents)

Exchanges remain as the most popular choice for cryptoasset storage amongst our institutional and VIP clients at 92.1%. When moving to self-storage, cold wallets are the second most favored choice, given their improved safety and control. Third-party custody services were the least popular option at 2.6%.

Table 3 - Use of decentralized exchanges according to respondents (in % of the total responses; June: 40 respondents; October: 68 respondents)

Have you ever used a decentralized exchanges (DEX)? | June 2019 | October 2019 |

|---|---|---|

Yes | 55.0% | 42.6% |

No | 45.0% | 57.4% |

Relative to the first survey, which was conducted in early June 2019, the share of respondents who have used decentralized exchanges has declined from 55% to 42.6%, a decrease of -11.4%.

Binance DEX launched last April, which likely drove a number of our clients to try out the platform just before the first survey’s distribution. In spite of the gradual increase in decentralized exchange volumes since the first survey, respondents appear to have shifted their focus away from experimenting with decentralized exchanges to alternative cryptoasset use-cases like lending, borrowing, and staking, as discussed in the next subsection.

1.3 On-chain crypto use-cases

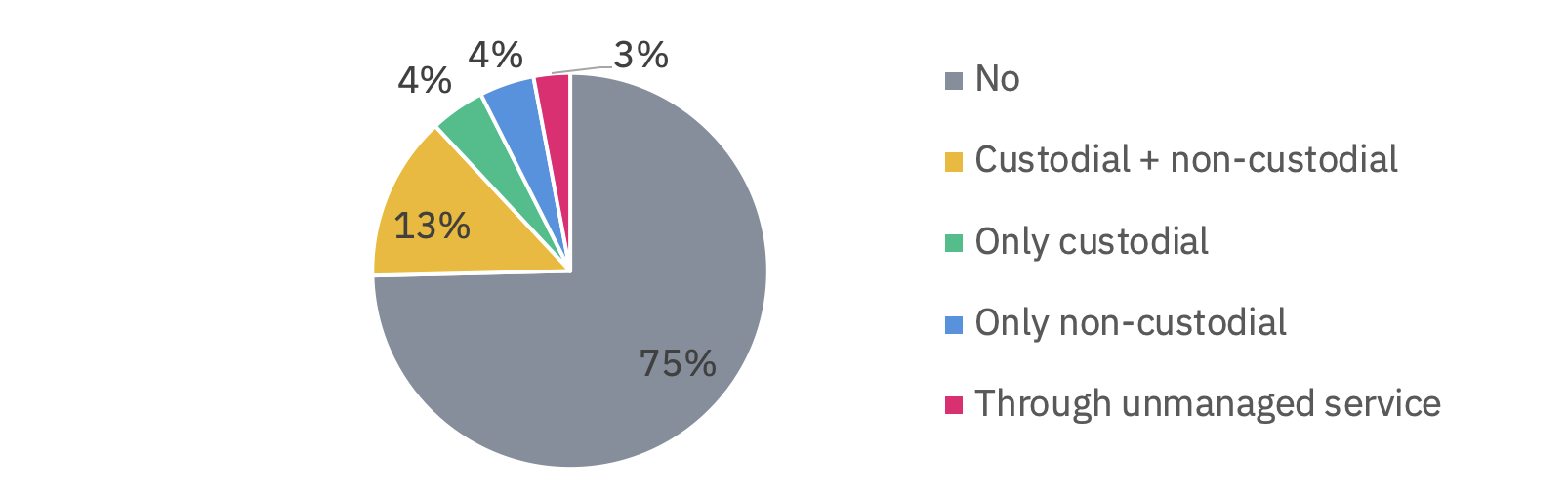

75% of respondents do not use crypto lending & borrowing services. On the remaining 25% that lend/borrow, most of the people use both custodial and non-custodial services. A few users indicated engaging in OTC-like lending practices, without displaying more additional information on whether these loans were collateralized.

Chart 6 - Lending/borrowing service use from respondents (in % of the total responses - 67 respondents)

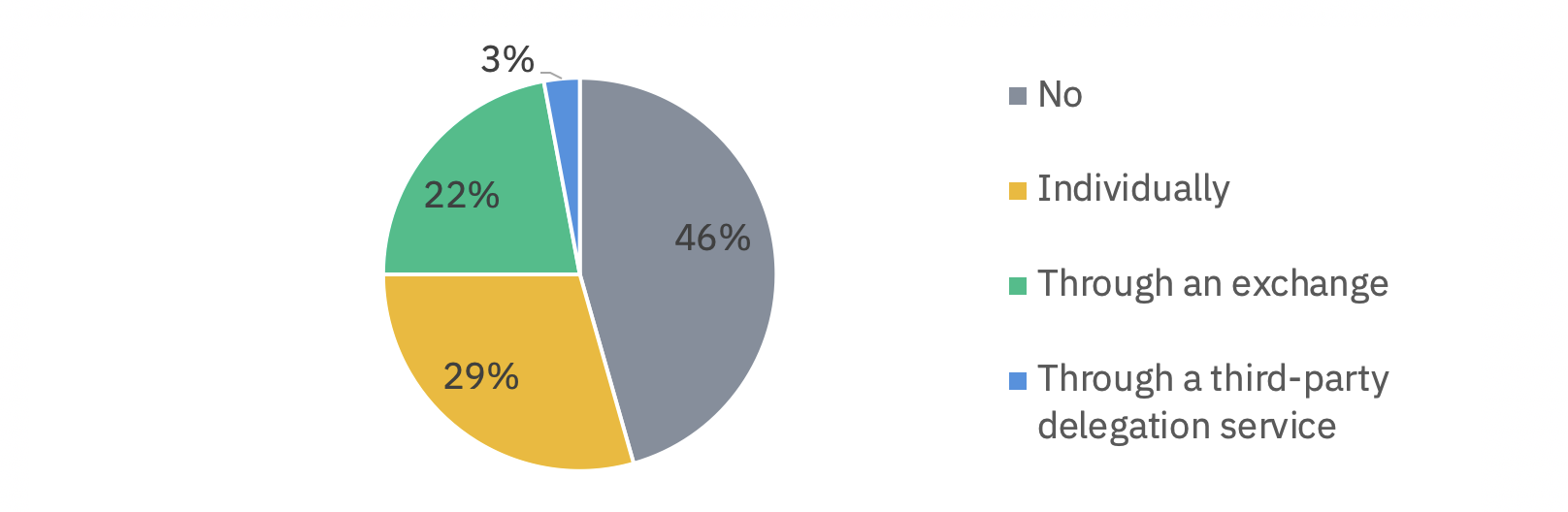

On the other hand, staking is more popular than lending, as 56% of the respondents stake some of their cryptoassets.

Chart 7 - Staking by respondents (in % of the total responses - 68 respondents)

29.4% of the respondents stake by themselves, i.e., interacting directly within the (first-layer) protocol. A quarter of the respondents rely on third-party services, and this sub-segment seems to be almost fully-dominated by exchanges (e.g., Binance, Kucoin).

Of the respondents that do engage in these passive income-generating (staking + lending) activities, 54% participate solely in staking, through an exchange and/or third-party delegation services (e.g., Binance Staking).

Potential reasons could include that staking is done natively at the protocol level of a blockchain while lending relies on trust: either from a third party (e.g., centralized lending services like Nexo) or a smart-contract (e.g., Compound, dYdX). On top of staking, the remaining 46% follow both strategies, utilizing both custodial and non-custodial options.

Regarding on-chain voting on platforms like Augur and MakerDAO, a mere 10% of the respondents ever used them, and they tended to be lower clients, based on the assets used for crypto-related activities. Some clients provided reasons such as the lack of liquidity (for Augur), the lack of interest in the governance process (for Maker), and the overall poor UX/UI of these services. This remains in line with the reasons provided regarding the use of decentralized exchanges. However, the level of interaction remains much lower than DEXs, as discussed in subsection 1.2.

2. Market views

2.1 Risks and potential growth drivers for the industry

In our survey, clients were requested to select exactly three risks and three growth drivers among respective lists of fifteen risks and twenty growth drivers.

Table 4 - Largest five risks according to client responses (60 respondents)

Largest risks | Percentage of clients |

|---|---|

(1) Platform-specific failure (e.g., exchange hack, etc.) | 48.3% |

(2) Tether ongoing legal issue | 43.3% |

(3) Global regulatory uncertainty | 38.3% |

(4) Lack of retail interest in altcoins | 30.0% |

(5) Domestic regulatory changes | 21.7% |

Nearly half of the clients ranked platform-specific failure (e.g., exchange hacks) as the top risk for the industry. Past exchange failures, such as Einstein Exchange or MtGox, remain a top concern as most trading activity remains on centralized platforms.

The Tether/USDT ongoing legal issue also is of concern to a significant portion (43.3%) of the institutional and VIP clients who participated in our survey. This is seen in some clients’ growing interest (see section 1) in alternative stablecoins such as BUSD.

Regarding regulations, respondents seem to be more wary of global regulatory uncertainty (43.3%) than potential domestic regulatory changes (21.7%). Potentially, it could relate to the relative ease of changing domestic registrations while facing the impossibility of not complying with regulations set at a supranational level.

The lack of retail interest in altcoins seems to be another critical risk for the industry. Many clients may be looking to achieve diversification within the crypto-space or to develop more complicated strategies that would require a broad range of liquid assets. Conversely, the least selected risks are summarized in table 5, as seen below.

Table 5 - Lowest five risks according to client responses (60 respondents)

Lowest risks | Percentage of clients |

|---|---|

(1) Privacy risk | 0.0% |

(2) Libra | 5.0% |

(3) Central Bank Digital Currencies (e.g., China’s CBDC) | 5.0% |

(4) Scalability issues | 8.33% |

(5) Individual security issues (e.g., phishing, SIM-swapping) | 10.0% |

Privacy risks and, to some extent, Libra and Central Bank Digital Currencies (CBDCs), which sparked debates related to privacy (e.g., US Congress3), were not considered as significant risks by most of the respondents. As a result, these ranked as the bottom 3 risks. Furthermore, neither scalability issues nor individual security issues were considered to be significant risks for the growth of the digital asset industry.

Table 6 - Largest six growth drivers according to client responses (60 respondents)

Largest growth drivers | Percentage of clients |

|---|---|

(1) Change in global & local regulations | 44.3% |

(2) Traditional brokerages offering crypto services (E-Trade, Fidelity Digital Assets) | 34.4% |

(3) Development of options contracts and other derivatives | 27.9% |

(3) Bitcoin ETFs | 27.9% |

(5) Libra (Facebook’s stablecoin initiative) | 19.7% |

(5) Central Bank Digital Currencies (CBDC) | 19.7% |

Unsurprisingly, changes in local and global regulations topped the growth driver list, with 44.3% of the participants selecting it. Once again, it remained in line with our past survey: in both June and October 2019, regulations were ranked both the most considerable risk and potential growth drivers for the future of the cryptocurrency and digital asset industry.

Traditional brokerages offering crypto-services were ranked, by more than a third of the clients, as one of the potential growth drivers for this industry. In comparison, it ranked as the third-largest growth driver in our previous survey.

New products such as the development of options contracts (e.g., Bakkt options) and other derivatives (e.g., Binance Futures’ perpetual contract) rank as high as Bitcoin ETFs for growth drivers. Digital currency initiatives by central banks4 and Libra also ranked relatively high, with nearly 20% of the participants considering it as top growth drivers.

Table 7 - Lowest five growth drivers according to client responses (60 respondents)

Lowest growth drivers | Percentage of clients |

|---|---|

(1) Privacy features (e.g., 2nd layer implementation or privacy coins) | 1.6% |

(2) Staking solutions | 1.6% |

(3) Private blockchains | 3.3% |

(4) Security tokens | 6.6% |

(5) Decentralized exchanges (e.g., Binance DEX) | 6.6% |

Same as a risk, privacy features also do not seem to spark much interest from a growth driver. Furthermore, despite increasing interest in the industry about decentralized exchanges, security tokens, and staking, these may not be considered growth drivers for the digital asset industry. While the low appeal for decentralized exchanges remains in line with what was discussed in section 1, staking was conducted by more than half of the clients despite staking solutions ranking as the second lowest growth driver for the industry. Hence, there might be a clear distinction between what is used and what will be a driving force for the growth of the crypto-ecosystem.

2.2 The future of Bitcoin and other large cryptoassets

In this subsection, we analyze the findings based on the expected prices for large cryptoassets, along with the expected Bitcoin market dominance at the end of 2019. Regarding the methodology, this survey was conducted from early October to the end of October. Clients were requested to input a price (in $ dollars) for December 31st 2019 (UTC time midnight).

Participant answers are summarized in table 5, displayed below.

Table 8 - Expected figures for prices and market dominance according to client responses

End of year figure | EOY expected value | EOY expected value - Quartile 1 | EOY expected value - Quartile 3 | October median |

|---|---|---|---|---|

Bitcoin market dominance | 69% | 62% | 72% | - |

Price of Bitcoin/BTC (USD) | 10,000 USD | 9,150 USD | 13,625 USD | 8,254 USD |

Price of Ether/ETH (USD) | 210 USD | 200 USD | 250 USD | 180 USD |

Price of XRP | 0.30 USD | 0.30 USD | 0.40 USD | 0.28 USD |

Based on the aggregated numbers provided by respondents (see table 5), these price predictions were optimistic (i.e., bullish), as median expectations were all above the median price levels during the data-collection period. However, these predictions remained quite conservative in their magnitude for an industry as volatile as the digital asset one.

Meanwhile, Bitcoin market dominance median prediction was around 69%, with little dispersion in the set of answers recorded. Compared to June 2019, people shifted upward their expectations related to the market dominance for Bitcoin for the end of the year. This echoes the fourth largest risk to clients, who quoted the lack of retail interest in the altcoin market as one of the critical risks for the development of the cryptoasset industry.

3. Conclusion and final comments

With this 2nd edition of our Institutional Market Insights report, we hope that the report shed some light on the attributes and market expectations from the largest participants in the cryptoasset industry. Despite only modest use of staking, decentralized exchanges, and lending, these products have become familiar names to industry participants. With the recent development of these products by Binance and other players, they are likely to gain broader adoption amongst clients, which we will highlight in future surveys. New derivatives such as swaps, options, and futures appear to be widely monitored by these participants, possibly owing to the high leverage available on these products and a more comprehensive range of sophisticated trading strategies that could be followed. Meanwhile, Bitcoin ETFs seemed to garner broad exposure, as their US regulatory approvals would allow on-boarding of many new traditional financial companies in the “Bitcoin rollercoaster”5. Talking about volatility, market participants remained moderately bullish for their forecast of the end of 2019. What close year-end prices will Santa bring in late December?

While stablecoins remained used by all participants and the meteoric growth in product offerings (new blockchains, new currencies, new collaterals) did not shake the previous status quo. USD Tether remains the go-to stablecoin, yet raising questions from many market participants on whether the emperor has clothes.

Following our review of the survey results, we now have five major questions for 2020:

Stablecoin evolution: Will Tether remain the king?

Regulations: How will regulations impact the future of this industry?

Central banks and corporate cryptocurrencies: Are CBDCs and Libra going to launch?

US-approved ETFs: Will a Bitcoin ETF be approved in the US?

Derivatives: Will options bring new trading opportunities for miners and other market participants?

Furthermore, with Bitcoin’s upcoming halving in 2020, it remains to be seen what will happen, from both a price and hashrate perspective, in the next four years in this industry, leading to 2024’s Bitcoin halving.

If you wish to trade large volumes with an efficient settlement procedure and competitive quotes, join Binance Trading on Telegram or send an email to tradedesk1@binance.com. Please reach out to one of the official traders on the channel, confirm your account and get ready to exchange the world. ↩↩

For the purpose of this report, clients involved in derivatives and spot trading on Binance.com, along with OTC users trading with Binance Trading were reached.↩

https://venturebeat.com/2019/10/23/u-s-congress-grills-mark-zuckerberg-on-facebooks-libra-privacy-elections-and-more/↩

Find our report about China’s CBDC there. https://research.binance.com/analysis/china-cbdc↩

See our Global Markets report from October 2019. https://research.binance.com/global-markets/october-2019↩